One of my 2017 mini objectives was to visit the Monzo office, meet the awesome team and see where the magic happens! If you haven’t heard of Monzo its a new bank, with ambitions to build the best bank on the planet. Have a look at their website and sign up – you will not be disappointed, and no I am not on commission!

I was lucky enough to grab one of the 50 tickets to attend Monzo OpenOffice event 31st Jan. The office was packed, there was more than 50 people, so I am guessing there was a few gatecrashers! I met some familiar faces from large banks, developers and many other people from all walks of life, keen to learn about Monzo’s special sauce. There was Pizza, drinks and the atmosphere was electric, people were genuinely excited to find out what is next in the Monzo story. The affinity to the Monzo brand, was apparent amongst the crowds of people clapping and cheering during the presentation – it was alike a micro scale Apple WWDC atmosphere.

Paul Rippon a co-founder and Deputy CEO, spoke about Monzo and their mobilisation journey in becoming a bank. The 5 stages of mobilisation Paul mentioned, are listed below – I have expanded on each point to add further context.

- Finance resource: Building up their capital investment and working capital so that they can meet their short term ambitions and long term strategic objectives. They plan to move to a new office in March. I do hope the have an office warming party

- People: Hiring awesomely talented people – everyone I met was truly altruistic and genuinely customer focused (plus their t-shirts looked super cool!). Having people like this in a organisation will be a great asset as Monzo expands, to ensure they keep their customer centric focus.

- Governance: Paul talked about the laborious process they had to go to gain a banking license. The European Parliament published on the 27th Jan a draft paper on its views about regulations on fintech. It is going to be interesting to see how regulation safeguards customers but allows the correct head space for innovation.

- Customer/Product: Building out customer base and refine product proposition. Monzos current proposition is prepaid and an awesome app. Monzo will move into the debit cards space in a few months, using staff as alpha testers until they have an acceptable stability – then they will open up to beta public testing. The debit card will provide an over draft facility and the usual direct debit, standing order and remittance. If the current proposition is anything to go by, its going to be exciting to see this proposition develop.

- IT: As with most banks, the borders between technology and banking are blurring. Monzo have created a great technology architecture stack as they have the advantage of starting from scratch. They use microservices using GO, native cloud and well defined interfaces that allows them to keep the cost of operations low and ensure flexibility to meet customers demands very quickly. This is not new technology – other companies that I have seen do this well include Spotify, Amazon and Netflix.

- Outsourcing: The build versus buy conundrum is an age long question. Do we buy it or do we build it? Monzo have clearly defined their core competencies and have clear guiding principles, so they build core capabilities in house, and outsource non core capabilities.

Conclusion

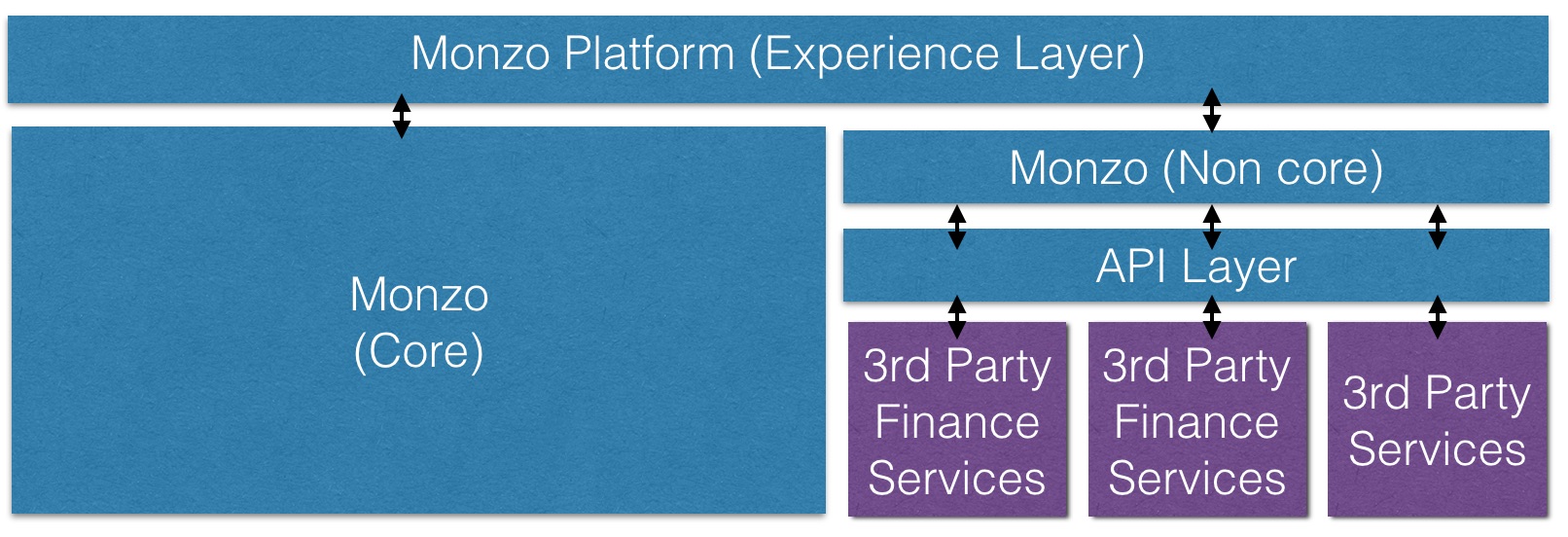

There seems to be new products and services being launched in fintech every day. Given money is an emotive subject and the inertia of switching accounts, fintechs will struggle to get mass market share and become a trusted brand. People may not like the big banks in some respects, however they know that their money is safe. However, I make an exception to the above statement with Monzo – I do believe Monzo has that special touch to potentially gain mass adoption and brand affinity. If I was to answer the question what is next for Monzo, I would say they will grow out capabilities and products steadily, making sure they seek feedback along the way. They will grow out their Monzo platform and own that experience layer, building lasting relationships with the customer. Their core proposition will be debit / prepaid, however they will innovate with virtual cards, tokenisation payments etc. As they build out their platform I envisage they will integrate with other financial services for non core activities. The customer journey will probably look like this: a customer requires a mortgage/loan, the customer will go to the Monzo platform, and Monzo will do the ‘behind the scenes’ complex number crunching, to get the the best deal for the customer. A win win revenue model, with partnership proposition and a multitude of FS, fintechs and other banks. I created this diagram on the train home from the event, to bring to life what is next in my eyes.

I am looking forward to 2017 & Monzo’s growth, watching them develop and launch new features, products and most of all magical customer-centric experiences.

Thanks for reading!

3 comments

Very good summary!

Amazing blog Bhavesh and thanks for coming! How about ‘3rd party non-financial service’ added to your diagram as well? 😉

Paul Rippon

Thank you for the comment 🙂 It was part of my thinking just never made it to the diagram. My thinking was PISP for purchasing and the tickets/ passes etc being available on the Monzo platform. As if by magic the diagram is updated! Also thank you for letting me take a selfie!